But why is the economy failing to generate prosperity as in earlier decades? Is it mainly down to Greenspan and Bernanke’s monetary excesses? Certainly, the latter has contributed to our contemporary stagnation, but perhaps if we look a little deeper, we might find an additional explanation. As I noted in a Comment of 6 January 2017, the golden era of US economic expansion was the ‘50s and ‘60s – but that era had begun to unravel somewhat, already, with the economic turbulence of the 70s. However, it was not so much Reagan’s fiscal or monetary policies that rescued a deteriorating situation in that earlier moment, but rather, it was plain old good fortune. The last giant oil fields with greater than 30-to-one, ‘energy-return’ on ‘energy-cost’ of exploitation, came on line in the 1980s: Alaska’s North Slope, Britain and Norway’s North Sea fields, and Siberia. Those events allowed the USA and the West generally to extend their growth another twenty years.

This week, there has been an avalanche of articles on Limits to Growth, just not titled so……. it’s almost as though the term is getting stuck in people’s throats, and are unable to pronounce them….

Alastair Crooke

This article by former British diplomat and MI6 ‘ranking figure’ Alastair Crooke, is an unpublished article I’ve lifted from the Automatic Earth…… as Raul Ilargi succinctly puts it…:

His arguments here are very close to much of what the Automatic Earth has been advocating for years [not to mention DTM’s…], both when it comes to our financial crisis and to our energy crisis. Our Primers section is full of articles on these issues written through the years. It’s a good thing other people pick up too on topics like EROEI, and understand you can’t run our modern, complex society on ‘net energy’ as low as what we get from any of our ‘new’ energy sources. It’s just not going to happen.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Alastair Crooke: We have an economic crisis – centred on the persistent elusiveness of real growth, rather than just monetised debt masquerading as ‘growth’ – and a political crisis, in which even ‘Davos man’, it seems, according to their own World Economic Forum polls, is anxious; losing his faith in ‘the system’ itself, and casting around for an explanation for what is occurring, or what exactly to do about it. Klaus Schwab, the founder of the WEF at Davos remarked before this year’s session, “People have become very emotionalized, this silent fear of what the new world will bring, we have populists here and we want to listen …”.

Dmitry Orlov, a Russian who was taken by his parents to the US at an early age, but who has returned regularly to his birthplace, draws on the Russian experience for his book, The Five Stages of Collapse. Orlov suggests that we are not just entering a transient moment of multiple political discontents, but rather that we are already in the early stages of something rather more profound. From his perspective that fuses his American experience with that of post Cold War Russia, he argues, that the five stages would tend to play out in sequence based on the breaching of particular boundaries of consensual faith and trust that groups of human beings vest in the institutions and systems they depend on for daily life. These boundaries run from the least personal (e.g. trust in banks and governments) to the most personal (faith in your local community, neighbours, and kin). It would be hard to avoid the thought – so evident at Davos – that even the elites now accept that Orlov’s first boundary has been breached.

But what is it? What is the deeper economic root to this malaise? The general thrust of Davos was that it was prosperity spread too unfairly that is at the core of the problem. Of course, causality is seldom unitary, or so simple. And no one answer suffices. In earlier Commentaries, I have suggested that global growth is so maddeningly elusive for the elites because the debt-driven ‘growth’ model (if it deserves the name ‘growth’) simply is not working. Not only is monetary expansion not working, it is actually aggravating the situation: Printing money simply has diluted down the stock of general purchasing power – through the creation of additional new, ‘empty’ money – with the latter being intermediated (i.e. whisked away) into the financial sector, to pump up asset values.

It is time to put away the Keynesian presumed ‘wealth effect’ of high asset prices. It belonged to an earlier era. In fact, high asset prices do trickle down. It is just that they trickle down into into higher cost of living expenditures (through return on capital dictates) for the majority of the population. A population which has seen no increase in their real incomes since 2005 – but which has witnessed higher rents, higher transport costs, higher education costs, higher medical costs; in short, higher prices for everything that has a capital overhead component. QE is eating into peoples’ discretionary income by inflating asset balloons, and is thus depressing growth – not raising it. And zero, and negative interest rates, may be keeping the huge avalanche overhang of debt on ‘life support’, but it is eviscerating savings income, and will do the same to pensions, unless concluded sharpish.

But beyond the spent force of monetary policy, we have noted that developed economies face separate, but equally formidable ‘headwinds’, of a (non-policy and secular) nature, impeding growth – from aging populations in China and the OECD, the winding down of China’s industrial revolution, and from technical innovation turning job-destructive, rather than job creative as a whole. Connected with this is shrinking world trade.

But why is the economy failing to generate prosperity as in earlier decades? Is it mainly down to Greenspan and Bernanke’s monetary excesses? Certainly, the latter has contributed to our contemporary stagnation, but perhaps if we look a little deeper, we might find an additional explanation. As I noted in a Comment of 6 January 2017, the golden era of US economic expansion was the ‘50s and ‘60s – but that era had begun to unravel somewhat, already, with the economic turbulence of the 70s. However, it was not so much Reagan’s fiscal or monetary policies that rescued a deteriorating situation in that earlier moment, but rather, it was plain old good fortune. The last giant oil fields with greater than 30-to-one, ‘energy-return’ on ‘energy-cost’ of exploitation, came on line in the 1980s: Alaska’s North Slope, Britain and Norway’s North Sea fields, and Siberia. Those events allowed the USA and the West generally to extend their growth another twenty years.

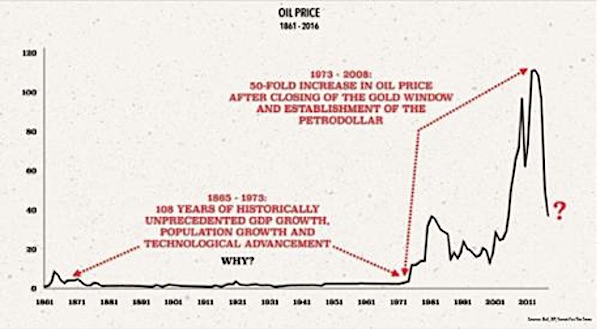

And, as that bounty tapered down around the year 2000, the system wobbled again, “and the viziers of the Fed ramped up their magical operations, led by the Grand Vizier (or “Maestro”) Alan Greenspan.” Some other key things happened though, at this point: firstly the cost of crude, which had been remarkably stable, in real terms, over many years, suddenly started its inexorable real-terms ascent. And from 2001, in the wake of the dot.com ‘bust’, government and other debt began to soar in a sharp trajectory upwards (now reaching $20 trillion). Also, around this time the US abandoned the gold standard, and the petro-dollar was born.

Source: Get It. Got It. Good, by Grant Williams

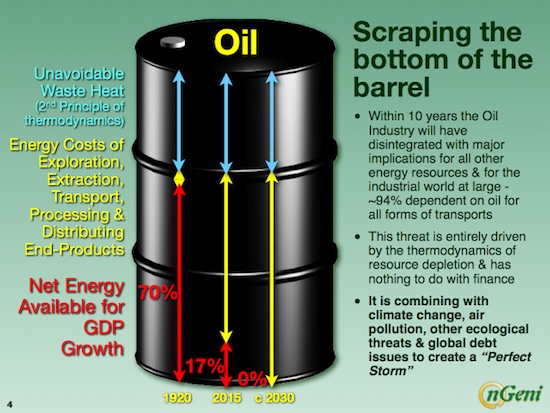

Well, the Hill’s Group, who are seasoned US oil industry engineers, led by B.W. Hill, tell us – following their last two years, or so, of research – that for purely thermodynamic reasons net energy delivered to the globalised industrial world (GIW) per barrel, by the oil industry (the IOCs) is rapidly trending to zero. Note that we are talking energy-cost of exploration, extraction and transport for the energy-return at final destination. We are not speaking of dollar costs, and we are speaking in aggregate. So why should this be important at all; and what has this to do with spiraling debt creation by the western Central Banks from around 2001?

The importance? Though we sometimes forget it, for we now are so habituated to it, is that energy is the economy. All of modernity, from industrial output and transportation, to how we live, derives from energy – and oil remains a key element to it. What we (the globalized industrial world) experienced in that golden era until the 70s, was economic growth fueled by an unprecedented 321% increase in net energy/head. The peak of 18GJ/head in around 1973 was actually of the order of some 40GJ/head for those who actually has access to oil at the time, which is to say, the industrialised fraction of the global population. The Hill’s Group research can be summarized visually as below (recall that these are costs expressed in energy, rather than dollars):

Source: http://cassandralegacy.blogspot.it/2016/07/some-reflections-on-twilight-of-oil-age.html

[This study was also covered here on Damnthematrix starting here…]

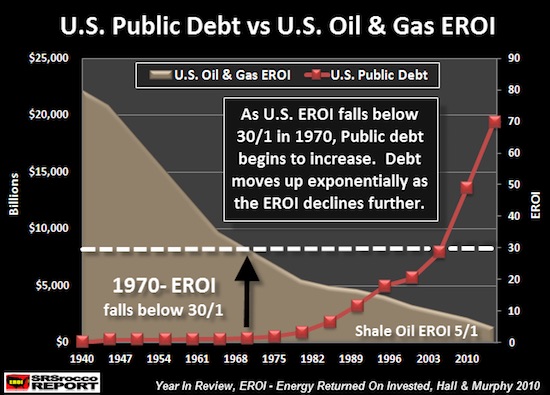

But as Steve St Angelo in the SRSrocco Reports states, the important thing to understand from these energy return on energy cost ratios or EROI, is that a minimum ratio value for a modern society is 20:1 (i.e. the net energy surplus available for GDP growth should be twenty times its cost of extraction). For citizens of an advanced society to enjoy a prosperous living, the EROI of energy needs to be much higher, closer to the 30:1 ratio. Well, if we look at the chart below, the U.S. oil and gas industry EROI fell below 30:1 some 46 years ago (after 1970):

Source: https://srsroccoreport.com/the-coming-breakdown-of-u-s-global-markets-explained-what-most-analysts-missed/

“You will notice two important trends in the chart above. When the U.S. EROI ratio was higher than 30:1, prior to 1970, U.S. public debt did not increase all that much. However, this changed after 1970, as the EROI continued to decline, public debt increased in an exponential fashion”. (St Angelo).

In short, the question begged by the Hill’s Group research is whether the reason for the explosion of government debt since 1970 is that central bankers (unconsciously), were trying to compensate for the lack of GDP stimulus deriving from the earlier net energy surplus. In effect, they switched from flagging energy-driven growth, to the new debt-driven growth model.

From a peak net surplus of around 40 GJ (in 1973), by 2012, the IOCs were beginning to consume more energy per barrel, in their own processes (from oil exploration to transport fuel deliveries at the petrol stations), than that which the barrel would deliver net to the globalized industrial world, in aggregate. We are now down below 4GJ per head, and dropping fast. (The Hill’s Group)

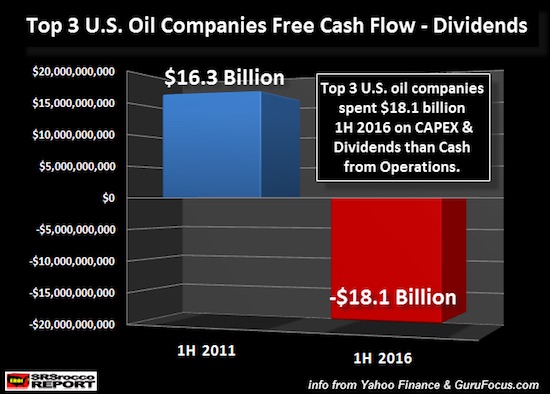

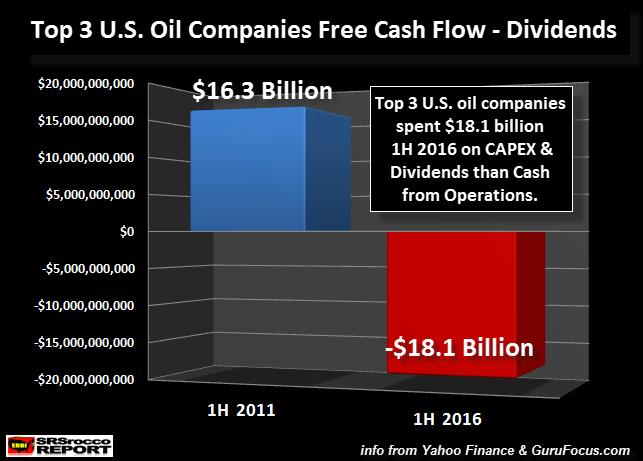

Is this analysis by the Hill’s Group too reductionist in attributing so much of the era of earlier western material prosperity to the big discoveries of ‘cheap’ oil, and the subsequent elusiveness of growth to the decline in net energy per barrel available for GDP growth? Are we in deep trouble now that the IOCs use more energy in their own processes, than they are able to deliver net to industrialised world? Maybe so. It is a controversial view, but we can see – in plain dollar terms – some tangible evidence fo rthe Hill’s Groups’ assertions:

(The top three U.S. oil companies, ExxonMobil, Chevron and ConocoPhillips: Cash from operations less Capex and dividends)

Briefly, what does this all mean? Well, the business model for the big three US IOCs does not look that great: Energy costs of course, are financial costs, too. In 2016, according to Yahoo Finance, the U.S. Energy Sector paid 86% of their operating income just to service the interest on the debt (i.e. to pay for those extraction costs). We have not run out of oil. This is not what the Hill’s Group is saying. Quite the reverse. What they are saying is the surplus energy (at a ratio of now less than 10:1) that derives from the oil that we have been using (after the energy-costs expended in retrieving it) – is now at a point that it can barely support our energy-driven ‘modernity’. Implicit in this analysis, is that our era of plenty was a one time, once off, event.

They are also saying that this implies that as modernity enters on a more severe energy ‘diet’, less surplus calories for their dollars – barely enough to keep the growth engine idling – then global demand for oil will decline, and the price will fall (quite the opposite of mainstream analysis which sees demand for oil growing. It is a vicious circle. If Hills are correct, a key balance has tipped. We may soon be spending more energy on getting the energy that is required to keep the cogs and wheels of modernity turning, than that same energy delivers in terms of calorie-equivalence. There is not much that either Mr Trump or the Europeans can do about this – other than seize the entire Persian Gulf. Transiting to renewables now, is perhaps too little, too late.

And America and Europe, no longer have the balance sheet ‘room’, for much further fiscal or monetary stimulus; and, in any event, the efficacy of such measures as drivers of ‘real economy’ growth, is open to question. It may mitigate the problem, but not solve it. No, the headwinds of net energy per barrel trending to zero, plus the other ‘secular’ dynamics mentioned above (demography, China slowing and technology turning job-destructive), form a formidable impediment – and therefore a huge political time bomb.

Back to Davos, and the question of ‘what to do’. Jamie Dimon, the CEO of JPMorgan Chase, warned that Europe needs to address disagreements spurring the rise of nationalist leaders. Dimon said he hoped European Union leaders would examine what caused the U.K. to vote to leave and then make changes. That hasn’t happened, and if nationalist politicians including France’s Marine Le Pen rise to power in elections across the region, “the euro zone may not survive”. “The bottom line is the region must become more competitive, Dimon said, which in simple economic terms means accept even lower wages. It also means major political overhauls: “I say this out of respect for the European people, but they’re going to have to change,” he said. “They may be forced by politics, they may be forced by new leadership.”

A race to the bottom in pay levels? Italy should undercut Romanian salaries? Maybe Chinese pay scales, too? This is politically naïve, and the globalist Establishment has only itself to blame for their conviction that there are no real options – save to divert more of the diminished prosperity towards the middle classes (Christine Lagarde), and to impose further austerity (Dimon). As we have tried to show, the era of prosperity for all, began to waver in the 70s in America, and started its more serious stall from 2001 onwards. The Establishment approach to this faltering of growth has been to kick the can down the road: ‘extend and pretend’ – monetised debt, zero, or negative, interest rates and the unceasing refrain that ‘recovery’ is around the corner.

It is precisely their ‘kicking the can’ of inflated asset values, reaching into every corner of life, hiking the cost of living, that has contributed to making Europe the leveraged, ‘high cost’, uncompetitive environment, that it now is. There is no practical way for Italians, for example, to compete with ‘low cost’ East Europe, or Asia, through a devaluation of the internal Italian price level without provoking major political push-back. This is the price of ‘extend and pretend’.

It has been claimed at Davos that the much derided ‘populists’ provide no real solutions. But, crucially, they do offer, firstly, the hope for ‘regime change’ – and, who knows, enough Europeans may be willing to take a punt on leaving the Euro, and accepting the consequences, whatever they may be. Would they be worse off? No one really knows. But at least the ‘populists’ can claim, secondly, that such a dramatic act would serve to escape from the suffocation of the status quo. ‘Davos man’ and woman disdain this particular appeal of ‘the populists’ at their peril.

{kind=link}

On the issue of resource depletion and why it leads to a Big Bang:

What is “US Public debt”? The US government has no money itself. It creates it into the non government domain. And so called Government debt is, in reality, “investor savings bonds”. That’s $20T misplaced. so what is the rest???

The wheels totally fell of in the 1970’s when the US broke from the gold standard and there was a oil crisis.

Except, they didn’t fall off. 30 more years of things being ok to good.

Until 2001. Then the wheels REALLY came off. A major stock market crash. A terrorism event that changed everything forever…

Except 7 more years of bumbling along, full bellies, and driving and flying everywhere. Now with smartphones.

Until 2008. Things really tanked. Everything came apart. We’re ruined for sure now. Banks, Frank-Dodd, debt, Dmitry Orlov, high oil prices, diminishing blah blah. Oil has peaked. Any day now, the drooling masses will finally understand.

Except 9 more years of bumbling along, full bellies, and driving and flying everywhere.

But NOW we’re doomed. EROEI is horrible, a lunatic is in charge, debt is finally too big (because we know those numbers), Dmitry Orlov said something, oh and so did Gail Tverberg.

The intellectual flaw here is that we the doomsayers don’t know what we don’t know. We didn’t imagine fracking or shale would be a thing. Then we didn’t imagine they would work somewhat. We didn’t imagine all the financial games, and if we could have, we wouldn’t have thought they’d work. And if we did, we wouldn’t have though they’d work for 15 years.

I don’t doubt the fundamentals. But I very much doubt our ability to predict much of anything, and it’s arrogant and ignorant to think we can. We’ve been wrong for 40+ years.

“But this time, for real.”

When you say we’ve been wrong for 40 plus years I think you are saying that the Limits to Growth team were wrong to predict that the world would reach hard limits by about now – 40 plus years after the publication of their seminal work.

I don’t think it was arrogant of those academics to publish their finding at all. Considering the potential fate that could disrupt society it was a very responsible thing to do.

And though we may (and should) debate the timingI don’t think it’s at all arrogant or ignorant to sensibly discuss their basic premise3 – that’s t’s impossible to maintain asymptotic growth in a closed system.

I do agree that nobody can predict with absolute certainty how the future will pan out, but considering what’s at stake I wouldn’t burn any heretical books that challenge Adam Smith’s satisfying theory that the economy will automatically defy any laws of physics.

Of all the debates that society should be having, considering the stakes, this is one that society has to have.

[You’ll have to excuse me GBell, I’m not too sure if your post was tongue-in-cheek or real. You could be remarking on some factors that weren’t foreseen and therefore have held the system together for longer than was expected?]

Chris –

You attempted to straw-man some of my statements. I will ignore that and clarify my original comments.

I’m reacting to the rhetoric and scare that has pervaded this community for decades. We’ve been drastically wrong about the timing, which means we may be wrong about the fundamentals. There’s a lot we don’t know, which means we shouldn’t be so sure of our conclusions.

Acknowledging that would lend some credibility to the things we’re saying today. I was publicly sounding the alarm in 2006 – do you think I have any credibility left today with those people I reached then?

By the way, according to the chart above, we went below the “critical EROEI to support modern society” (20:1) in the late 1980’s!

No GBell. I’m simply respectfully disagreeing with you.

The Limits to Growth team were ridiculed for getting their projected timing wrong but that didn’t ever de-legitimise their basic premise in my view. In fact I think their projection was amazingly close to the mark. Our world is in disarray over both resource depletion and biosphere pollution.

Personally I predicted a disruption to the world economy in 2014, but my certainty on that timing was not absolute. I won’t suffer a failure of nerve and disagree with my own mathematics because the oil corporations tell us ‘the world is swimming in oil’ or because depletion of oil reserves means that hydrocarbons are being fracked from under our feet.

That said, any movement has to be careful not to be persuaded by its own rhetoric. Many advocates of Peak Oil thought geology when they should have been thinking economy. I don’t think the Peak Oil movement (just like the unconventional oil industry itself) could have predicted the Arabian strategy to dump oil prices.

The world will never run out of oil, in time it will run out of affordable oil… along with a range of other resources.

Actually Chris, the CoR didn’t get its timing wrong….. all along it predicted a collapse mid 21st Century.

Re never running out of oil…..

Of the estimated 22 trillion barrels of oil (liquids) in the ground so far we’ve used up 1 trillion. This sounds like there are some 21 trillion barrels left unless we look at how it is formed and what it would take to get at it. The graph shows it all. Most of the oil under our feet would use up more energy in its extraction than we could usefully get from it… even if we didn’t cook the planet in the process.

A bit like phosphorus. Every green plant has phosphorus, and green plants are just about everywhere. But we need mineable deposits, and they are very finite. 80 years max I saw. Oil is far from the only problem.

22 trillion Chris…? I thought there were maybe 3……

If my memory serves me correctly the 22 trillion comes from Kurt Cobb. Of that he argued that about 6 trillion could theoretically be extracted a pinch, but not necessarily with a positive ERoEI. For the most part we are talking tiny little puddles and hydrocarbons locked up in porous rock structures.

It’s a bit like aluminium, which comprises 8 percent of the world’s crust. The aluminium that mineable is just a tiny fraction of that massive total. Nobody is going to mine the aluminium that’s in your garden clay.

Fracking and shale USED TO BE a thing…….. that is the point of the collapsing ERoEI. I heard Chris Martenson say that the Bakken has already well and truly peaked, and that other big one is peaking now….

Gail did mention divine intervention…… 😀